“Robo advisors will manage over $5 trillion in 10-years.” Have you seen headlines like this? According to the reports, robo advisors are so wonderful, they’re going to overtake the world and make it a better place to invest. Imagine, if you can, flowers and cute Bambis everywhere!

In reality, robo advisors are not really “advisors” but rather online software powered by algorithms. How does it work?

(Audio) Here’s what the “big money” is buying + A $3.5 million Portfolio Report Card

After a person inputs their age, risk preferences, financial information, and other related data, the software spits out a recommended portfolio allocation. Generally, robo advisors use broadly diversified ETFs that own U.S stocks (NYSEARCA:SCHB), international stocks (NYSEARCA:VEA), emerging market stocks (NYSEARCA:VWO), and bonds (NYSEARCA:BND) as portfolio building blocks. While there may be slight variations between the portfolios recommended by different robo advisors, all of them use algorithms based around Modern Portfolio Theory or some hybrid version of it.

Most robo advisors are U.S. based, but similar iterations also exist in Australia, Canada, and Europe.

Despite the robo advisor hype, there are plenty of reasons to be skeptical. Let’s examine just three reasons why robo advisors are hazardous to your wealth.

Robo Advisors are Untested

The latest generation of VC-backed robo advisors were launched at the perfect time; during a sustained period of rising stock prices. As a result, today’s robo advisors lack experience when it comes to managing assets during sustained periods of market turbulence and falling stocks prices (NYSEARCA:DVY).

In the aftermath of the 2008 financial crisis, Warren Buffett warned, “Beware of geeks bearing formulas.” He said that because Wall Street’s beautifully designed risk models (algorithms) contributed to the mass murder of $22 trillion.

Today, instead of listening to Buffett’s good advice, a growing population of novices have gullibly entrusted their life savings to robo advisors. In other words, they’ve been tricked by the clean looking apps and interface that are powered by unproven spaghetti.

During the next stock market meltdown, it’s a sure bet that robo built portfolios will get slaughtered. Why? Because it’s in the very DNA (and history) of smart-sounding algorithms to get killed by angry financial markets.

Robo Advisors are Unaccountable

In an effort to solve problems, technology has introduced new problems that are sometimes more complex than the original problem.

For example, Google’s driverless cars are a great idea for people like me who hate to drive. But who’s liable when the driverless car hits a pedestrian? Is it the automobile’s owner? Is it Google? Or is it the pedestrian?

Since robo advisors aren’t really “advisors” but rather software programs, who’s responsible when the investment portfolio recommended by the robo goes haywire – or worse yet – blows up? Who are the responsible individuals hiding behind the software code? And why aren’t robo clients given their direct contact information?

In truth, the programmers behind robo software may have experience at coding, but they don’t have experience in financial matters impacting people’s lives . Robos recognize this flaw and a certain ones have desperately adopted a hybrid model of humans and software. But when software is still driving the final decisions, the advice rendered always comes up short. In other words, a pig with good-looking lipstick is still a pig.

The idea that robos could ever approach or serve in the role as a “fiduciary” is a total farce. It’s akin to arguing a wheelchair is capable taking the Hippocratic oath between itself and its patients.

Although robos are registered with the Securities and Exchange Commission (SEC), they are not fiduciaries nor do they fit under the traditional standard applied to human registered investment advisors (RIA). And therein hides the problem for the investing public: Robos lack accountability for the investment decisions they make on your behalf.

Robo Advisors Overcharge

The notion that robo advisors are inexpensive is widespread but wholly untrue. While robos may cost less compared to traditional human RIAs, they are substantially more expensive versus ETFguide’s investment advice service.

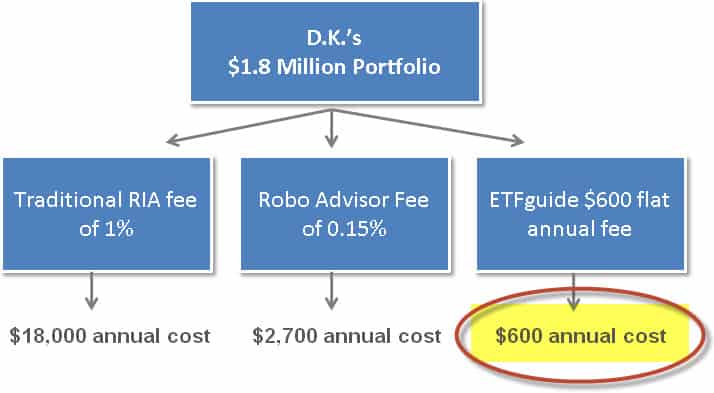

Below is a real life example of D.K., a married couple with a $1.8 million portfolio, who chose ETFguide’s investment advice service over competing choices.

The traditional RIA wanted to soak D.K. for $18,000 in annual asset fees while the robo wanted to charge $2,700. After adding fund expense ratios and trading costs to the tab, the compounding cost and outlay for both of these options over a long-period of time becomes a substantial amount of money.

Instead, D.K. chose ETFguide’s Investment Advice program for just $600 annually – or 96% less compared to the traditional RIA and an amazing 78% less compared to robos.

Not only does D.K. get unhindered access to a licensed human advisor with ETFguide, but they always talk to an advisor who shares our same passion for transparent, tax-friendly, and low cost investing. D.K. will never be charged any asset fees – ever. Furthermore, D.K. doesn’t forfeit personalized investment advice rendered by a qualified and licensed human advisor.

Summary

I reject the silly propaganda that robo advisors are a positive development for the investing public. How could anyone in their right mind embrace the deformed viewpoint that faceless and de-personalized investment advice is good?

Moreover, robos are unproven during sustained periods of falling markets and I predict that 90% of them will fold during the next bear market.

Especially worrisome is the fact that robos lack accountability for the investment advice they give. Robos allow software programmers with zero investment experience to camouflage themselves behind code.

Finally, robos are an expensive choice compared to better alternatives like ETFguide’s Investment Advice. Unlike robos, we recognize that human advisors are an essential ingredient to long-term investment success and we gladly work with advisors who adopt our low-cost business philosophy. “Gentlemen, to save our businesses from ruin…we must reduce expenses,” is how we think and operate.

I hate robo advisors and you should too!