It’s commonly and incorrectly presumed that people with large investment portfolios are smart investors. But as counterintuitive as it may sound, this false presumption is simply not true. How do I know?

Because I’ve analyzed and graded many multi-million dollar investment portfolios ($27 million is the largest one I’ve graded so far this year) using my Portfolio Report Card grading system – and many of these very portfolios have flunked on important factors like cost, risk, diversification, and performance.

(Audio) How the $700 Million Man Lost his Fortune + Getting Higher Returns with Lower Risk

What’s does it mean when seven figure portfolios are flunking? That being a good saver doesn’t automatically make a person a good investor. On the other hand, combining a good savings habit along with a militant approach toward investment costs, risk, diversification, and taxes should lead to the satisfactory performance.

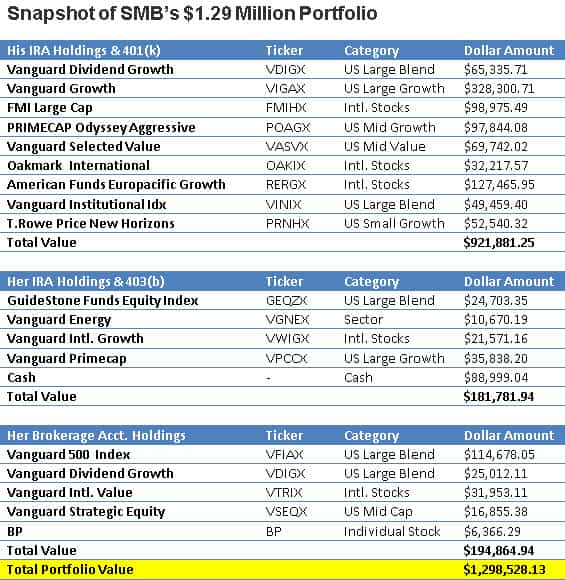

My latest Portfolio Report Card is for a married couple, SMB, living in Houston, TX. Both are in their early 50s and they asked me to grade their combined $1.29 million investment portfolio which consists of two traditional IRAs, two Roth IRAs, a Roth 401(k), a 403(b), a 401(k) plan, and a brokerage account.

SMB told me they are aggressive growth investors and generating income is a low priority at this stage of their investment plan. The entire $1.29 million portfolio is self-managed.

What kind of grade does SMB’s portfolio get? Let’s analyze it together.

Cost

The investment costs you bear today compound over time and will erode your investment returns. And that’s why reducing the negative impact of trading commissions, fund fees, and other frictional costs is something the prudent investor carefully does.

SMB’s combined portfolio hold 17 mutual funds, 1 individual stock, and cash. The asset weighted annual fund expenses on the mutual funds are 0.39% vs. 0.20% for our index benchmarks. Put another way, SMB’s fund costs are almost twice as high vs. the benchmark. This portfolio still has too much fat and could use a diet.

Diversification

A truly diversified investment portfolio will always have broad market exposure to the five major asset classes: Stocks, bonds, commodities, real estate, and cash. How does SMB’s portfolio do?

SMB’s portfolio owns mutual funds investing in U.S. and international stocks (NYSEARCA:EFA), and cash. However, the portfolio misses direct exposure to major asset classes like bonds (NYSEARCA:AGG), commodities (NYSEARCA:DBC), and real estate (NYSEARCA:ICF). Put another way, SMB has a two-asset class portfolio which comes up far short of being genuinely diversified.

Risk

Your investment portfolio’s risk character should always be 100% compatible with your capacity for risk and volatility along with your unique financial circumstances, liquidity requirements, and age. Furthermore, all portfolios – large, small, and in between – should have a margin of safety.

The overall asset mix of SMB’s combined portfolio is the following: 92.2% stocks (NYSEARCA:DIA) and 7.8% cash. Even for early 50s aggressive investors, this asset mix tilts on the hyper-aggressive side. Put another way, a 20% to 40% market decline would subject the total portfolio to potential market losses of $208,000 to $416,000.

Tax Efficiency

What you sow is what you reap. And a smartly designed investment portfolio takes proactive steps at cutting the threat of taxes. Owning tax-efficient investment vehicles and having proper asset location are two easy steps.

Around 85% of SMB’s portfolio is invested in tax-deferred retirement accounts and they have no outstanding loan balances or pre-mature retirement distributions that have increased their tax bill.

Their taxable brokerage account has exposure to Vanguard stock funds with reasonable tax-cost ratios. Overall, SMB’s portfolio does outstanding at tax-efficiency.

Performance

Investment performance will always reveal whether an investment portfolio is architecturally strong or weak. And satisfactory performance is a direct result of controlling cost, taxes, risk and diversification.

SMB’s portfolio grew $91,159 (+8.1%) from June 2014 to June 2015 vs. a gain of +9.1% for the index benchmark matching their same asset mix. Although they slight underperformed the benchmark, it wasn’t by much and their portfolio’s one-year performance is satisfactory.

The Final Grade

SMB’s final Portfolio Report Card grade is “B” (good). They scored best in the following categories: tax-efficiency, and performance.

However, this portfolio flunked in the risk category. Their 92% exposure to equities isn’t age appropriate and is well beyond just aggressive – it’s hyper-aggressive! SMB’s margin of safety is non-existent and a market decline of 20% to 40% market decline would subject their portfolio to significant market losses.

Likewise, a lack of diversified exposure to major asset classes like real estate, commodities, and bonds is a missing ingredient.

What about cost? Although SMB owns several low cost index funds, the higher cost funds they own unnecessarily elevate the total portfolio’s fund expenses. Cutting investment cost further should boost SMB’s long-term net returns.

Will SMB take corrective action to fix the weaknesses in their portfolio? If they do, I’m confident they’ll reach their financial goals with less risk, less cost, and less stress.

Ron DeLegge is the Founder and Chief Portfolio Strategist at ETFguide. He’s inventor of the Portfolio Report Card which helps people to identify the strengths and weaknesses of their investment account, IRA, and 401(k) plan.