Actively managed portfolios are not a device of nefarious origin. And neither is it a “dead exercise” as the vox populi has declared. Nevertheless, to be successful at active investing, there are some big time hurdles. Before we discuss these obstacles, let’s first clarify the term “active investor.”

An “active investor” is somebody who is managing a portfolio of investments that is different, in both composition and character, compared to benchmark indexes within the same asset class. I rather like how William F. Sharpe, Nobel Prize winner in economics, described it.

(Podcast) Is Momentum Investing a Good Strategy for You?

He wrote:

“An active investor is one who is not passive. His or her portfolio will different from that of the passive managers at some or all times. Because active managers usually act on perceptions of mispricings, and because such perceptions change relatively frequently, such managers tend to trade fairly frequently – hence the term ‘active.'”

The active investor’s goal, of course, is that the effort of being different from “passive” index investors will produce index-beating performance. It’s a noble goal, but one that goes unrealized more often that not.

The Hurdles

Among the biggest obstacles for active investors are costs. Since active and passive returns are the exact same before costs, and because active managers bear greater costs, the after-cost returns from active management, in aggregate, will be lower compared to passive indexes. These higher costs for active management come in various forms, from higher fund expense ratios to higher brokerage transaction costs and the tax burden of those transactions.

Be in the Know! Get complimentary ETF Guides delivered to your inbox

Then too, there are psychological hurdles.

Active investors and managers, for instance, can be victims of herd mentality. How many active investors were overweight technology stocks in late 1999 right before the dotcom bust? Other times, active investors are so stubbornly fixed on a certain approach, they get blindsided by their own self-wisdom. Bruce Berkowtiz at Fairholme Funds (Nasdaq:FAIRX) has been bludgeoned by Sears (Nasdaq:SHLD), yet he continues to buy more and more stock of the beleaguered retailer on every seeming dip. Bruce is a good example of the self-destruction that embroils some active investors when they get in too deep and they want to keep going even deeper.

And let’s not forget the sad group of active investors that were overweight some of the greatest financial atrocities of our generation like Enron, MCI Worldcom, and Bernie Madoff’s scam.

For the super-rate success story in active investment management, there are many more failures.

Proper Context

Do the countless challenges facing active investors mean that you should absolutely avoid funds that attempt to outperform the market? Not necessarily. In fact, there’s always an outside chance you might find a certain stock or fund manager that smokes the performance of stock market indexes. But then too, the more probable outcome is that you won’t encounter such a rosy, feel-good scenario.

So, if you’re going to be an active investor – whether it’s buying individual stocks, trading futures or options contracts, betting on fund managers who are shooting for alpha, or arbitraging vintage cars – it’s vital that you do it right. And I believe the only right way to be an active investor is to assign a fixed and limited portion of your total assets to this strategy. What is the right percentage that should be committed to active strategies?

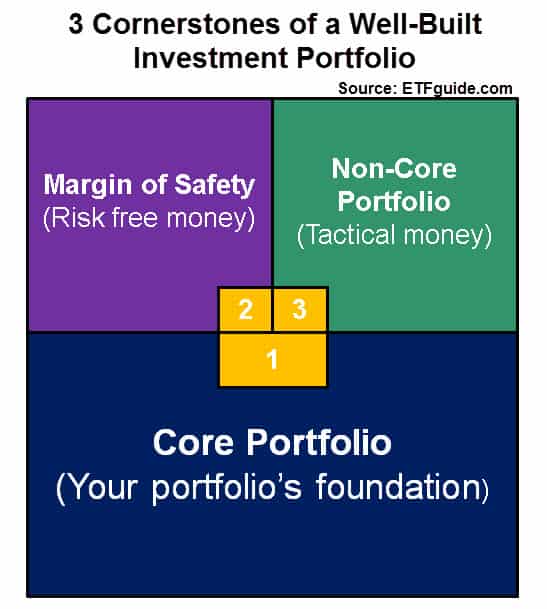

If the core or foundation of your investment portfolio is at least 51% or more of your portfolio’s total assets, that leaves 49% of your money for the other two buckets: Your non-core portfolio and your margin of safety. The latter represents the capital that is earmarked for a permanent buffer of money with zero volatility and no chance of loss. After you determine how much of your money you want committed to safety, the rest can be allocated to your non-core portfolio – the ideal setting and proper context for the active investor to run wild.

At best, any wonderful gains you achieved because you “beat the market” will lift your total portfolio’s performance. At worst, if you fail to achieve market beating results, the sub-standard performance will be contained to your non-core portfolio. Meanwhile, your core portfolio – which is 100% indexed across stocks, bonds, real estate, and commodities – should deliver the hard to beat results of “passive” investing.